Giving is something I am passionate about. According to The Five Love Languages by Gary Chapman, gifts is one of my top love languages. I believe giving is so much more than just the monetary or financial value of what is given. I believe it unlocks the greater ability inside of us to help others and actually prefer to see others prosper over ourselves. As Christmas nears, my wife and I continually contemplate how to gift more experiences to our kids over just “stuff.” Two of our favorites in the Billings area are Steep World and Red Lodge Mountain, just to name a couple.

In the world of charitable giving, not only can we seek out ways to help others, but we can maximize our giving through the power of organizations that have a primary purpose or mission of doing so. In giving to these organizations, we can multiply our effect on others by supporting causes that we can do more with together, instead of separately. As Christians, we are further called in the Bible to bring our tithes into the storehouse(church) of the first fruits of our increase.

“Bring all the tithes into the storehouse, that there may be food in my house, and try me now in this,” says the Lord of hosts, “if I will not open for you the windows of heaven and pour out for you such blessing that there will not be room enough to receive it.”

Malachi 3:10

“Honor the Lord with your possessions, and with the firstfruits of all your increase.”

Proverbs 3:9

I am also passionate about ways that utilize our investments to make our giving go even farther. By taking advantage of strategic giving options, we can create opportunities for tax savings that ultimately lead to more money going to more purposes. Although not a popular opinion, the IRS does have a soft spot for charitable giving, and if utilized correctly, can offer significant tax savings. While I believe a true gift should be made regardless of the tax implications, a true steward will look to maximize what he has been given, Matthew 25:14-30

Three Effective Methods for Tax-Smart Tithing

Transferring Publicly Traded Securities

Just to make sure there is no one lost in the jargon, a publicly traded security is an investment that is available to purchase on the open market through an exchange and held in a brokerage account. The most common examples of publicly traded securities are stocks, mutual funds, and ETFs.

Publicly traded securities are one of the most popular ways to invest in the stock or fixed income markets because of their efficiency, transparency, and transferability. If you are at a point in your life where you are investing, your investments are probably not the first asset you think of when you are considering when and how much to tithe to your church. However, to fully understand the power of giving with this kind of asset, let’s first look at how they are taxed.

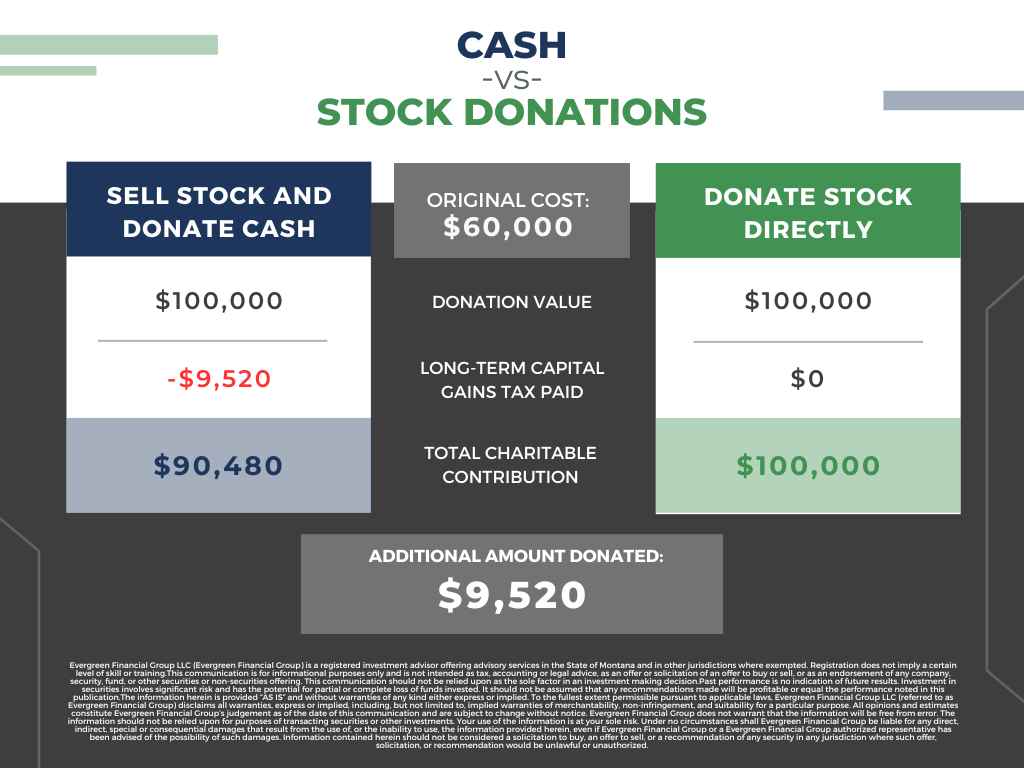

The first consideration when looking at any investments you are considering giving is what type of account they are held in. In this example, you will want to look at any securities that you hold in a non-IRA or non-retirement account. Examples of good accounts to donate from include individual, joint, or living trust accounts. If these investments are held in non-retirement accounts, gains and losses are reported upon sale according to capital gains rules, which is the amount sold, also known as proceeds, minus the amount paid, also known as basis. In the event of a sale, the amount of any gain or loss is then reported on your tax form and is taxed at capital gains rates. In this example, we will look at long-term capital gain tax rates, which are currently 0%, 15%, or 20% if you’ve owned the security for over a year.

If you’ve owned a stock, mutual fund, or ETF in a non-retirement account for a significant length of time, chances are you’ve seen this particular investment increase in value above the original purchase price. This is known as an unrealized gain. Since you haven’t yet sold the asset, there are no capital gains you have to report. While selling the investment in your own account would trigger this gain to be reported as a realized gain, you also have the ability to potentially transfer the investment in kind to your church or charity without having to pay for the gain yourself.

Transferring an investment in kind to a church creates an advantage because, if your church qualifies as a public charity, you are eligible to transfer not only the full market value of the investment, but also the unrealized gain attached to the security. The advantage this creates is that your church, because of tax exempt status, can sell the investment without any tax implication, taking full advantage of the appreciation and convert the investment into cash to use for its purposes, if desired.

Further, this creates an additional tax advantage for the donor. The donor of an appreciated security can deduct the Fair Market Value of the investment at the time of donation up to 30% of their Adjusted Gross Income. Because there was no capital gains tax paid on the unrealized gain of the security, the taxable gain on the security turns into a tax savings in the form of a charitable deduction on the entire value of the donated security, not just what was paid for it initially. Whoohoo!

Let’s look at a visual example of this to help understand the concept easier:

Even though this strategy is fairly straightforward in nature, there are a few items to check on before going ahead and putting it into action:

- You have to hold the security for over a year. As mentioned above, the tax savings on transfer to your church or charity is only applicable if the gain is a long-term capital gain, which is an investment that has been held for over a year.

- The church or receiving organization must hold a brokerage account to receive the investment shares. Publicly traded securities such as stocks, mutual funds or ETFs are transferred through the Depository Trust and Clearing Corporation(DTCC) and must be sent to a specific account at a specific brokerage firm. If your church or charity has set this up, they will be able to give you the account name, account number and firm where the church’s brokerage account is held.

Utilizing a Donor Advised Fund

Using a Donor Advised Fund(DAF) to contribute to your church can be as equally effective of a tool as directly transferring securities, but with more flexibility. A DAF can also be an alternative to giving when your church doesn’t have a brokerage account. While we could discuss the many features of a DAF in much more depth, we will focus on the strategic tax efficiencies they can provide for this example.

A DAF is a pool of money set aside for charitable purposes that you control. You can decide what, when and how much goes in and goes out. Essentially, you can think of it as your own charity. A DAF account can be set up at many different brokerage firms and can be invested in publicly traded securities, just like any other brokerage account. A key feature with a DAF is that the donor to a DAF receives a tax deduction on the amount of the donation into the DAF, not necessarily what goes out to the end recipient. Another key term is that the money going out of a DAF is referred to as a grant, similar in terminology to a grant that would be received from a foundation or endowment.

Since the IRS views a DAF as a tax exempt entity, a donor can gift publicly traded securities in kind to a DAF, receive a tax deduction, and avoid the potential capital gains tax, just like in the case of transferring directly to a church or charity as we discussed above. These investments can then be sold in the DAF, and transferred out to a church in cash via a grant from the DAF.

Again, the key tax consideration is that the tax benefits are calculated based on when the donation is received by the DAF, not the end recipient/organization. Securities will fluctuate based on market conditions, so it is important to keep in mind that the exact donation value won’t be known until after the transfer is complete. In addition, any appreciation that the security has after it’s donated to the DAF is not deductible. However, any investment gains after the donation can still be granted to your church or other organization and further increase your gift’s total impact.

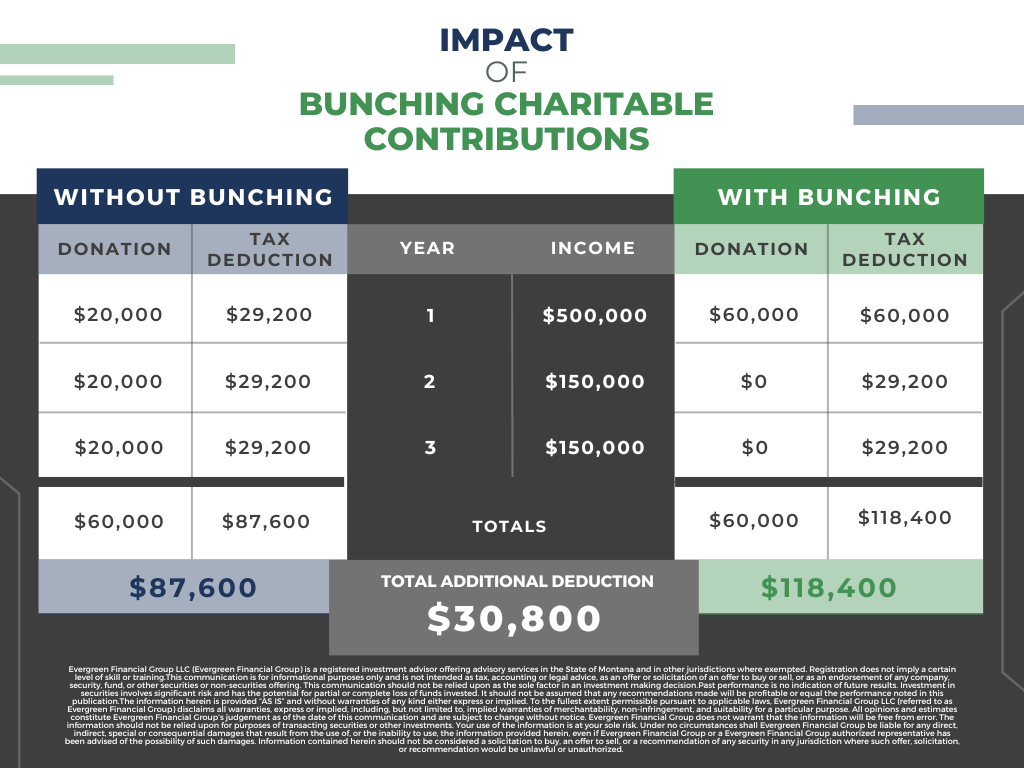

As mentioned above, DAFs can provide additional flexibility on what, when and how much to donate. In many cases, a security will simply be donated, sold, and then almost immediately granted to the end recipient/organization. However, a DAF can work great if you want to adopt a strategy called “bunching”. Bunching allows the owner of a DAF to donate a large amount of securities in one tax year to achieve a large deduction in that tax year. This is advantageous if you have an abnormally large income year and need to offset it to reduce your tax burden.

Here is an example. As you can see below, the table below shows the difference between a $20,000/yr donation made either per year for 3 years or $60,000 all at once and then granted over 3 years. Because of the increase in the marginal tax rate as income rises, a lump sum $60,000 donation creates a tax savings in the large income year while still allowing the donor to make the same $20,000 annual gift/grant amount to the organization. In the years where the standard deduction exceeds the itemized deduction, the standard deduction is still taken even if the charitable contribution is $0. At the time of this writing, the standard deduction for 2024 is $29,200 for those married filing a joint tax return.

Because of the control and flexibility the DAF provides, a bunching strategy can be an effective worthwhile tool for both realizing large tax savings and accomplishing charitable giving goals.

There is one final caveat to make with DAFs, which is to be mindful of fees, especially when working with a small amount. DAFs generally work best with contributions that are larger, more spread out, or both. Since the majority of brokerage firms charge an administrative fee for the work of managing DAFs, being mindful of these fees in relation to the value of the DAF becomes important. If you are planning on just making a one-time, small donation, it might not make sense to use a DAF.

Utilizing Qualified Charitable Distributions

The third and simplest way of tax-efficient tithing is by using Qualified Charitable Distributions(QCDs). QCDs have a few different requirements, but they are fairly straightforward. Let’s take a look.

If you are over 70½ and have a Traditional, SIMPLE, or SEP IRA, using a QCD to give all or most of your tithe or other charitable contribution can create an additional tax advantage. It is also most effective if you typically take the standard deduction when filing your taxes and do not itemize.

First, let’s look at the order of how your income and deductions are listed on your tax return. Note that this simple example is for educational purposes and is not considered tax advice.

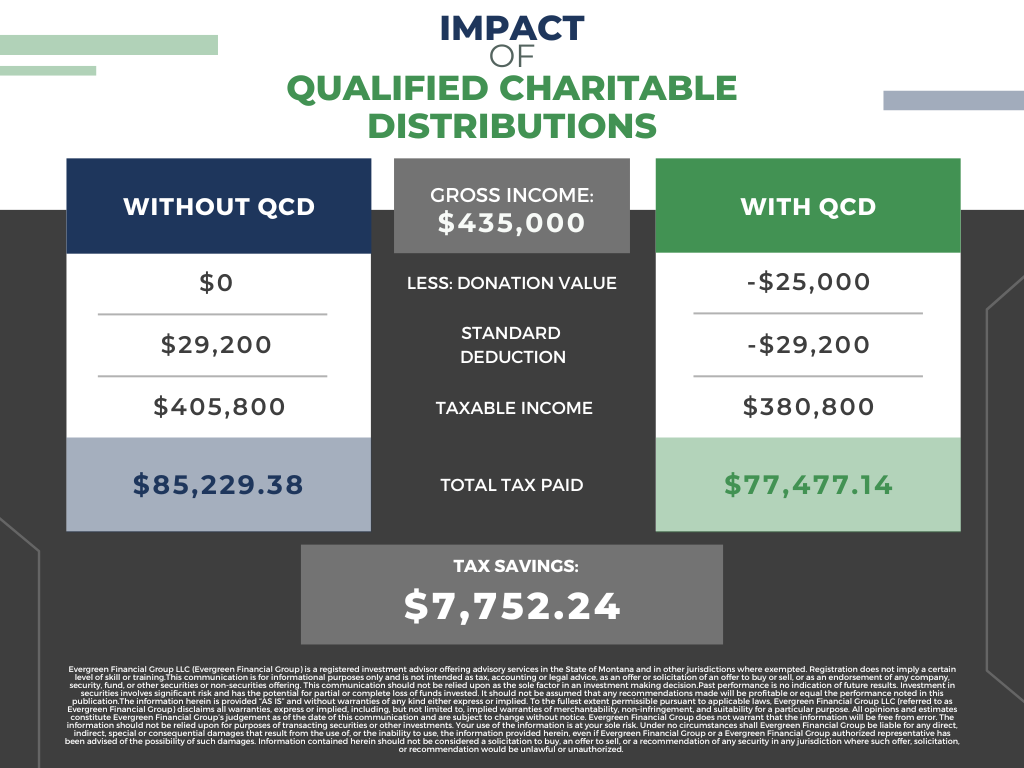

The simple formula for calculating your income taxes is: Gross Income – Standard Deduction = Taxable Income. Currently, the standard deduction for a couple filing a married filing joint(MFJ) tax return in 2024 is $29,200.

The main advantage of a QCD is that it allows you to capitalize on two forms of tax savings. In addition to taking the full standard deduction, you also get to exclude the amount QCD from your gross income if done properly. One requirement of a QCD is that it must be given directly from your IRA to the qualified charity. Because this exclusion occurs before deductions are taken, it actually becomes an additional reduction in income while still allowing the full standard deduction to be taken. This translates into a larger tax savings! Yay!

There are many benefits to using QCDs as donation tools. One of these is that they can be given in cash, unlike our first two examples. Because funds in an IRA grow tax-deferred, investments can be sold off proportionately to the amount being withdrawn from the IRA without incurring capital gains. This makes it easy when it comes to giving as you can give an exact amount without worrying about transfer values or market fluctuation.

A second benefit when using QCDs is that QCDs count towards satisfying any Required Minimum Distributions(RMD). Under current law, RMDs must be withdrawn from the account in the year the owner reaches age 73. This age is scheduled to increase to 75 in 2033.

One of the requirements of a QCD is that they must be given directly to the charity from the IRA. While this can occasionally take some extra time when filling out distribution paperwork, many custodial firms offer the ability to get a checkbook and write a check out directly to the charity in cash. This essentially creates a “giving account” that donations can be made from. This also makes it easy when keeping track of donations for tax reporting.

All in all, tithing and charitable giving can be done in a tax-efficient manner that provides not only tax advantages for the donor, but also maximizes donation dollars to go the farthest. Using the tools discussed above, such as directly transferring appreciated securities, donor-advised funds, and Qualified Charitable Distributions create a win-win situation for all parties involved. Be sure to consult a qualified tax professional and financial planner before making any charitable contributions to make sure it fits into your overall financial plan.

Interested in working with us?

Schedule A CallKnow someone who might be interested in working with us?

Fill out our referral formThis content is developed from sources believed to be providing accurate information. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security. Evergreen Financial Group, LLC is a registered investment advisor offering advisory services in Montana and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training. This communication is for informational purposes only and is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision. All opinions and estimates constitute Evergreen Financial Group’s judgement as of the date of this communication and are subject to change without notice. Evergreen Financial Group does not warrant that the information will be free from error. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk.