If you’re anything like me and my family, the end of summer marked a stark transition back to reality as my kids went back to school. While the added structure and schedule are a welcome change after the summer craziness, we were flooded with a multitude of demands coming at us: Sports schedules, after-school activities, homework, volunteer committees, coaching, school supplies, etc. While none of these requests individually were an extreme commitment or time or energy, the sum total of everything together proved to be a bit overwhelming.

The financial industry, and even more guilty, the media, loves to create stress over finances. By creating a flurry of confusing jargon and complex ideas, they essentially create a state of paralysis for many consumers. I’ve said it before, and I’ll say it again—the media doesn’t exist to help you succeed financially. They want to create a sense of fear and helplessness that gets more clicks and views. This is what pays their salaries.

Thankfully, we don’t have to exist in a state of panic, fear, or even worry. By focusing on what matters most, we can simplify and de-stress our investing experience. In this post, we’ll discuss the purpose of investing, what investment ideas matter, and how to prioritize how your money gets invested.

Why Invest in the First Place?

Investing is simply using your money to make money. While investing can take many forms, the idea is to create more than what you started with. As we advance through stages of life, we encounter inflation, higher costs, and more demands for our money. Investing is one of the surefire ways to make sure the money you have lasts for as long as you need it—and then some.

For many, investing may seem like a foreign concept that is more confusing than intuitive. For ease of simplicity, we will use publicly traded investments to illustrate a few concepts.

Understanding Investing Through Publicly Traded Investments

When you buy a share of a publicly traded stock, you become a fractional owner of the company you bought. As the owner, you get to share in the profits and growth of the company proportionate to the number of shares of stock you own. If you are a business owner or have ever watched a small business as it grows, you know you are creating more value in that business than what it had to begin with. In the same way, investing is a way that an owner participates in the increase of the business he or she owns.

With the invention of electronic trading and exchanges, we as a worldwide economy have been able to facilitate the buying and selling of publicly traded investments with the push of a button. One of the biggest benefits to individual investors is that they can now get access to the worldwide marketplace of investments at a very low cost. Previously, an investor would have to contact a broker to place a trade for them and pay a high commission on both the buy and sell side. However, it is now possible to own a globally diversified portfolio and pay just a fraction of a percent in ongoing fees.

While you may have heard of terms like Price-Earnings ratio, Earnings per Share, or Dividend Yield, these are just ways of evaluating investments. These are important to professionals who manage investments for a living. However, the main focus of an individual investor should be to find the most efficient and effective way to own the best-suited investments for you long-term.

What Investment Ideas Matter and In What Stage of Life?

While there are cases where an individual’s age and stage of life might not match their investment portfolio, the number one factor involved in investment success is time. 90% of Warren Buffet’s wealth was created after he turned 65. If an investor wants to experience success with their investment ideas, it’s imperative time is allowed to reap the benefits.

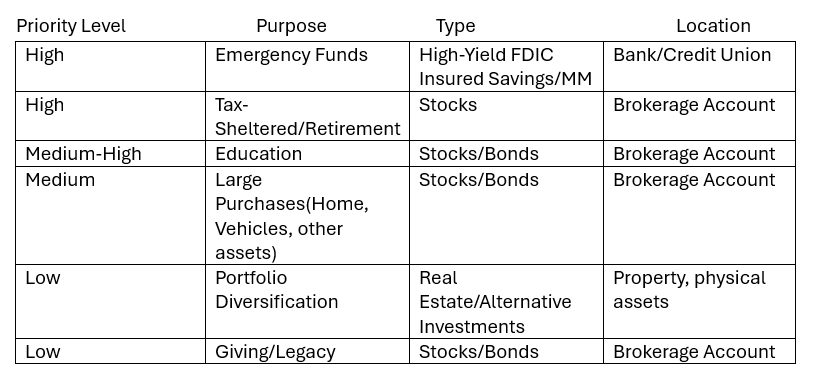

While every investor’s situation will vary, here is a typical framework to start with and watch your portfolio grow:

Setting Yourself Up for Success: Making Financial Priorities

Goal setting is the most important part of the process. When setting goals, it is important to always prioritize your own goals first. Just like a flight attendant’s simple reminder “make sure you put your own mask on before helping someone else”, the same is true for investing. I’ve seen many people try to invest for others before they invest for themselves. While it’s a noble thought, unlike paying off college loans, there are no “finance your retirement” loans available at your local bank. Here are our recommended list of priorities:

- High Priority: Prioritizing the long-term goals of your retirement and future should be a priority of its own, only after making sure you have enough cash in the bank to cover an emergency or two. This not only secures a future for you/your spouse, but it also creates a foundation from which your other investing can be built. If you are on track for a stable, well-funded retirement portfolio, you can simply take on more risk in other areas without derailing your personal future. However, if you don’t have a stable base to work from, you simply can’t afford to take unnecessary risks in other areas.

- Medium Priority: Other medium-priority goals can come after you’ve made adequate headway in securing your future. Goals like your child’s education, or buying a new house/car can be started once you’ve seen success in your highest priority goals. The underlying investment ideas for these goals can vary but typically will involve a combination of high and low risk investments. Since these goals will also have a medium-term timeframe, it is important to create a portfolio with the same level of risk. This combination creates less volatility than a more aggressive portfolio, allowing for a higher probability of the funds being available when they are needed most.

- Low Priority: On the lowest end of the goal priority scale are the goals that are the “icing on the cake”. Examples of two lower-priority goals include alternative investments and giving. Alternative investment ideas can be a great way to add additional diversification, but should only be explored if an individual is already on track to fund their high-priority goals. Studies have shown that even a simple, well-diversified portfolio will allow an individual to achieve their long-term goals. However, if there are certain opportunities or areas of the market that you would like to explore, alternative investments could be a fit in certain cases.

Another example of a low-priority goal would be giving. This can be intra-family giving or legacy planning. Keep in mind that I didn’t say this was of low importance. Giving is a great source of joy for many(myself included), but this again should not take the place of higher priority goals.

Diving Into Charitable Giving

One exception to giving being a low priority goal is charitable giving. For example, if you believe in tithing, giving to your church is not just an option, but an instruction we are given in the Bible. Malachi 3:10 reads, “ Bring all the tithes into the storehouse so there will be enough food in my Temple. If you do,” says the Lord of Heaven’s Armies, “I will open the windows of heaven for you. I will pour out a blessing so great you won’t have enough room to take it in! Try it! Put me to the test!” While I believe in discipline and wise financial planning, there is simply nothing that can match the return of giving to God. The great thing about giving into the Kingdom of God is that we cannot outgive him. If we give out of the right heart and not just to get something in return, we will see blessings come on our lives that we can’t measure in the world’s terms. If our creator is exhorting us to give more and put him to the test, I am going to do what he says! Giving to God is the highest priority goal!

Simplify Your Investment Ideas with Evergreen Financial Group

If you feel overwhelmed with all of the financial jargon being thrown at you, you’re not alone. While it may seem like there is no way to wade through all of the news headlines, turmoil, and stress, we can help. Taking the time to research seemingly complicated information is a win in itself!

Let us simplify the rest for you, contact us today to get started.

Interested in working with us?

Schedule A CallKnow someone who might be interested in working with us?

Fill out our referral formThis content is developed from sources believed to be providing accurate information. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security. Evergreen Financial Group, LLC is a registered investment advisor offering advisory services in Montana and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training. This communication is for informational purposes only and is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision. All opinions and estimates constitute Evergreen Financial Group’s judgement as of the date of this communication and are subject to change without notice. Evergreen Financial Group does not warrant that the information will be free from error. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk.