My kids are getting their first taste of “real” roller coasters this year. This March, we took a trip to Universal Studios to celebrate Spring Break. My son, who is 8, was brave enough to try the Velocicoaster for the first time. I remember seeing his combined reaction of joy, excitement, joy and terror as we accelerated downward and he felt the G forces hit his whole body. Naturally, he came to quickly understand how roller coasters work and decided to not go back right away. However, after a couple hour hiatus, he was ready to again; now knowing what to expect. We are headed to Silverwood later this summer and I anticipate he will be a little more prepared for what lies ahead.

As we think about the world of investing and the stock market, it’s easy to associate the market with a roller coaster ride. However, with some preparation, foreknowledge, and a little experience, investing can feel less like a roller coaster and more like a predictable pattern of events. In this post, we’ll break down 5 ways you can be prepared for what to expect both before and during a stock market crash.

Hold more than just an emergency fund

Having a healthy emergency fund in place is a pretty standard regimen as it relates to financial advice. However, not many realize the importance of having more cash available than just the next 3-6 months of expenses. To gain true insulation from the whims and cycles of the market, a full 2 years worth of expenses is a much healthier buffer that can help to make even the worst of economies more bearable.

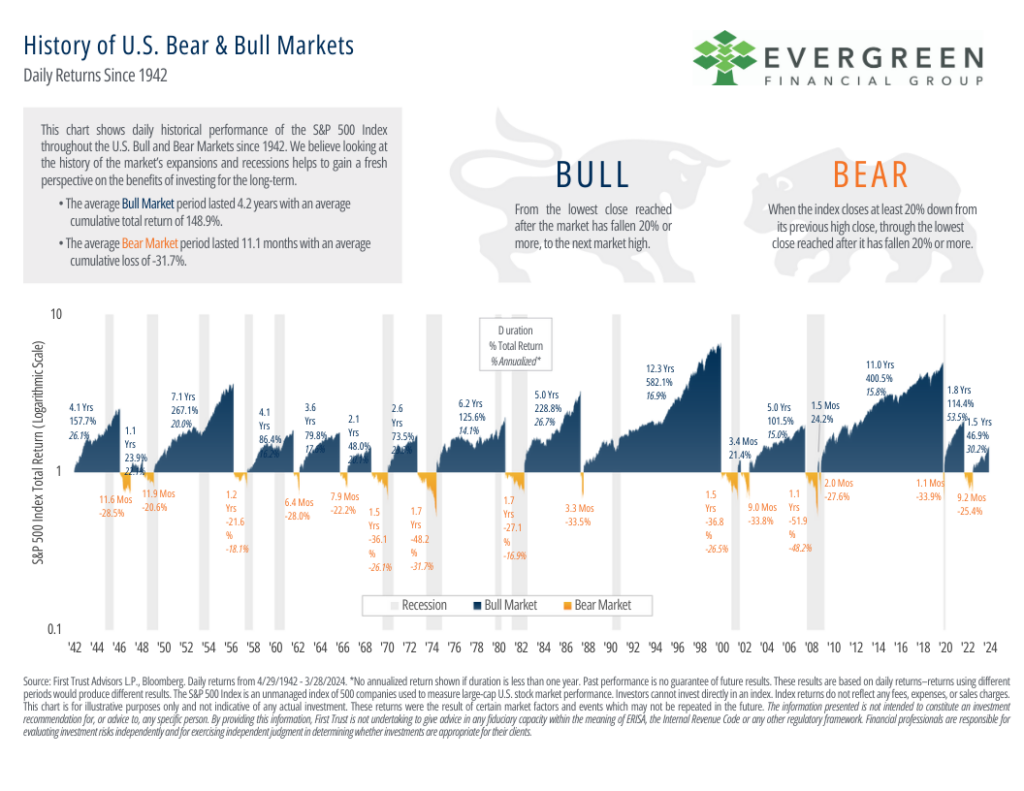

Why 2 years of expenses? Looking back over the past 80+ years, history has proven that a 2 year window allows for a fairly reliable gauge to ride out many of the market’s up-down cycles. While some bear markets have certainly proven to be longer than 2 years, there are still many cases where a 2-year timeframe has been sufficient to provide protection from selling and dipping into the wrong investments at the wrong time.

As you can tell on the chart below, not only do the majority of down markets last less than 2 years, but they are also much less severe than their bull market counterparts. This also brings up one of the fallacies of market timing. In order to truly be able to be successful in market timing, you have to guess right twice – once when you get out, and once when you get back in. A much more proven, sound strategy is to have your fund of 2 years of expenses in place to be able to withstand a prolonged down cycle.

There are many intangible benefits that also result from having a well-funded emergency fund. While many people feel the pinch during down markets and cut back on discretionary spending(as you should during a down market), simply knowing ahead of time that you’ve prepared and have the funds available allows you to have peace of mind knowing that you are ready for this. Further, you know that you are not creating permanent losses by selling investments below where you bought them. You are simply withdrawing cash or cash equivalents that were never subject to market risk in the first place. Check out our post and recent webinar on the 4 Key Asset Buckets in Retirement for a full breakdown of how to structure retirement income withdrawals.

Review Your Tax Allocation

Many people understand the concept of asset allocation – ensuring that your investments hold the proper proportions of major asset classes, including stocks, bonds, cash, real estate, and commodities. However, Tax Allocation is also an important part of using the right types of accounts for the right types of investments. For instance, since Roth IRAs and Roth 401ks allow for tax-free qualified withdrawals, higher growth investments are the best type of asset to own in these accounts. On the other hand, tax-exempt bonds are best used in non-qualified accounts such as Individual, Joint, and Revocable Trust account types.

While there are obvious financial and tax benefits to having the right assets in the right accounts, there is another benefit at play with Tax Allocation. In the world of Behavioral Finance, we as humans experience something called Mental Accounting. We naturally associate different parts of our assets and belongings to different compartments in our brain. While this can be helpful in some cases, it can also lead to detrimental actions in dire or bleak situations. For example, let’s say someone’s grandmother passed away and left a stock she owned from a company she worked for 20 years. Upon receiving the account, the person inheriting it continues to hold the investment because it had sentimental value to his grandmother, although he has no emergency fund and he could sell it with no consequence due to the step up in basis rules.

As we can see from the outside, there are multiple good reasons to sell the stock and diversify the account into a more disciplined strategy. However, the mental accounting bias is blocking this type of more rational thinking from taking place.

We can all fall victim to a similar type of bias due to our emotional decision making. However, one of the benefits to Tax Allocation is that we can use it to make good mental accounting decisions. If we have our most aggressive investment allocation in our longest-term accounts, we realize that we don’t need the money in that respective account for a long time anyway. This can make us more encouraged to “ride out the storm” and not sell an asset that has probably seen a short-term decline but has more potential to go up in the long-term.

Meet Regularly With Your Financial Advisor

If you aren’t already doing so, meeting regularly with a trusted financial advisor is key to being prepared for a market downturn. If you aren’t working with an experienced CERTIFIED FINANCIAL PLANNER ®, check out our post on 5 Essential Tips for Choosing the Right Financial Advisor.

If you’ve ever engaged in sports or an activity that requires training or practice to master, you know the value of a good coach. In the same way, a trusted financial advisor will help you to not only understand what’s going on in our economic world, but also how to encourage you on how to keep going when times are tough. More than just a pep talk, a good advisor will help you to gain perspective on your situation and “see the forest for the trees” when you don’t know how else to move forward.

Another benefit to working with a trusted financial advisor is how he or she can help you filter the important information from information that won’t benefit you. We all know that the media doesn’t get paid to publish news to make us feel financially confident. It is exactly the opposite. If the media can get you to react to an emotional market headline, they’ve accomplished their mission. Conversely, a good financial advisor will help you to understand the context around news/market headlines and help you to filter out the information that is just to benefit the media. This will not only keep your emotions in check, it will also help you to make better financial decisions in times of crisis.

A third benefit to working with a trusted advisor is that you and they are on the same team. Any good teammate wants to see you succeed and will work with you to accomplish your shared goals. More than just someone looking to get a paycheck, a good financial advisor will know more about you than just another business colleague and will have a desire to put your best interests first. If you don’t have this type of relationship with your advisor, make sure to find someone who is a fiduciary.

Don’t Stop Investing New Money

If you are actively making contributions to your investments, don’t stop putting new money in because of the potential of a market downturn. There are very few times that we as humans would ever not buy something when it goes on sale. However, we treat the market as a worse deal when it goes down. In fact, we often buy more only when it goes up. This simply is a bad financial decision based on emotion. The fact is, continuing to buy during market dips can be on the fastest ways to recover from a market downturn.

Another bad financial decision many investors make during down markets is to decrease their risk tolerance. While it can be unnerving to see an investment portfolio go down more than you expect, the time to decrease exposure to risk should’ve been done before the downturn happens. Further, decreasing risk tolerance should only be done based on one’s financial situation, not simply based on the perceived market or economic outlook. Personal factors such as time until retirement, health concerns, or moving to a new location are all valid reasons to decrease one’s risk tolerance. However, issues such as political rumors or a financial influencer’s economic predictions should not be used as a basis for your portfolio’s risk tolerance.

Rebalance When Opportunities Arise

Finally, one of the few beneficial actions that should be taken during a down market is to rebalance when opportunities arise. Working in conjunction with a trusted financial advisor, a rebalance of your portfolio to it’s target allocation can be a favorable move. However, it is important to evaluate a potential rebalance carefully. If the costs and tax implications are low, it might make sense to rebalance. However, if it will result in more taxes or costs than what you might potentially make up for, staying put might be a better choice.

Rebalancing at a lower market level has multiple benefits. Studies have shown that asset allocation, not security selection, drive the majority of a portfolio’s return. This means that the overall proportion of a portfolio’s exposure to the broad asset classe s(stocks, bonds, etc) is more important than the individual holdings of the portfolio. By rebalancing at opportune times, we keep this allocation in balance with our stated goals and risk tolerance.

Discipline is another benefit from a strategic rebalance. We know that rebalancing is part of a good ongoing investment management strategy, and a market downturn doesn’t change this. While typical rebalancing should be done in a disciplined, periodic manner, a strategic rebalance can be worked into this existing framework, and essentially just “accelerated” due to the market conditions at hand. Notice that I didn’t say reallocate your portfolio, as that involves a change in the asset allocation that we just discussed.

If, after careful evaluation, you and your advisor decide that a rebalance is not a good decision, don’t fret. The stock market has recovered from 100% of the corrections it has EVER experienced. This is a good reason to be confident in better days ahead.

Interested in working with us?

Schedule A CallKnow someone who might be interested in working with us?

Fill out our referral formThis content is developed from sources believed to be providing accurate information. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security. Evergreen Financial Group, LLC is a registered investment advisor offering advisory services in Montana and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training. This communication is for informational purposes only and is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision. All opinions and estimates constitute Evergreen Financial Group’s judgement as of the date of this communication and are subject to change without notice. Evergreen Financial Group does not warrant that the information will be free from error. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk.