The thought of planning a trip evokes many different emotions for many different types of people. Some love the feeling of crafting the perfectly designed experience, with side trips, excursions, local culture, food, and multiple other luxuries. On the other hand, other people can’t stand the thought of having to put hours of work into something that will cost money and result in them longing for a vacation from their vacation after returning home.

At any rate, trip planning takes time, money, and thoughtfulness in order to properly fulfill what its planner hopes to accomplish. In the same way, retirement planning involves the same aspects of planning, but with two very important distinctions. In retirement planning, you don’t know how long the “trip” will last, and you don’t know how much it will cost.

In this post, we’ll explore 5 strategies the best financial planners use to help those both before and in retirement to maximize the time that they will be spending in their golden years.

What Is a Retirement Planner?

While “retirement planner” is not a commonly recognized title in the financial industry, here are some of the best titles to look for to help get the right expertise and advice for retirement:

- Certified Financial Planner® (CFP®)

- Chartered Financial Consultant® (ChFC®)

- Retirement Income Certified Professional® (RICP®)

All of these roles carry a level of knowledge and expertise in helping those nearing or in retirement to navigate all of the various decisions and considerations necessary.

One common misconception in retirement planning is that it’s easier to pull money out of investments than it is to put money in. However, the opposite is true. Due to all of the various withdrawal requirements, tax implications, healthcare costs, government programs, and other factors, it truly becomes a juggling act to properly manage and wisely steward retirement assets. Here are some strategies some of the best retirement planners use:

1. A Withdrawal Strategy

The first strategy the best retirement planners use is to craft a reasonable and sustainable withdrawal strategy. There are multiple studies, including the 4% rule and guardrails, that have shown how to structure an income stream from an investment portfolio while not eroding the corpus.

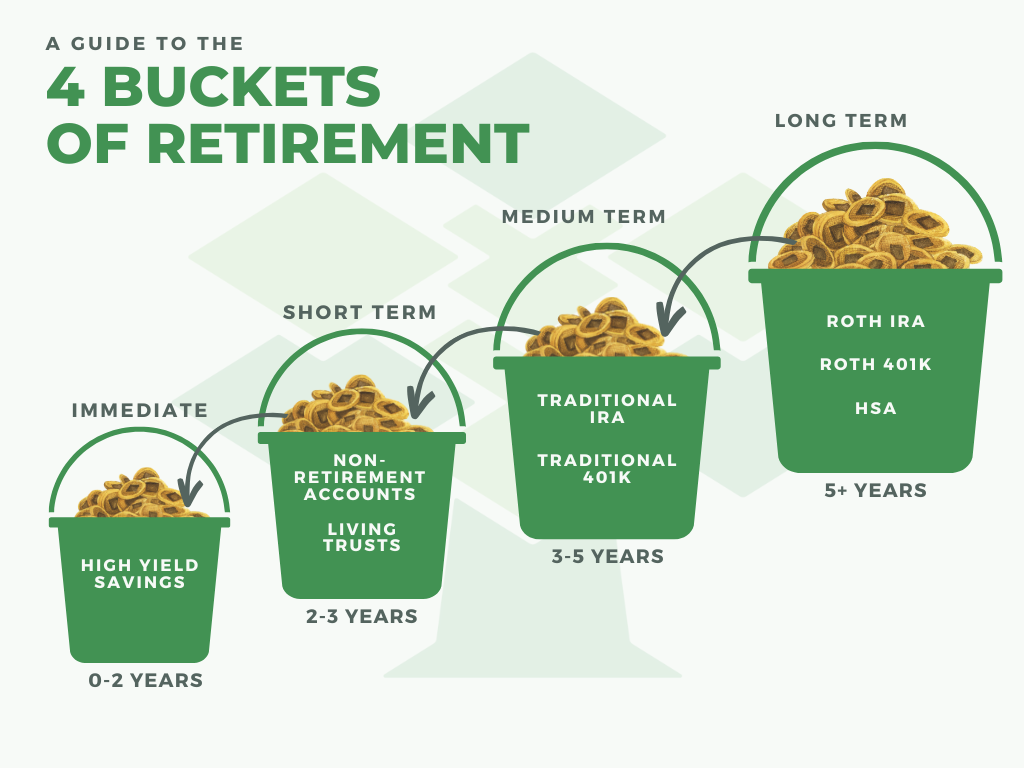

Here at Evergreen, we structure our retirement portfolios using the bucket strategy framework. It allows for an intuitive, flexible model that can be adjusted based on market conditions, lifestyle changes, and any other needs that come up for an investor in retirement. For a more detailed explanation of this strategy, check our previous blog post and webinar.

Another important factor in creating a sustainable retirement withdrawal strategy is coordination with Social Security and Medicare. Many retirees are aware of these important milestones when arriving in retirement yet few understand just how interrelated they are with retirement income.

One particular factor that arises frequently with Medicare is the Income Related Monthly Adjustment Amount, or IRMAA for short. In essence, IRMAA is an additional surcharge that is added to Medicare Premiums when income surpasses certain thresholds. This arises most often when retirees reach the age that they have to begin taking Required Minimum Distributions. For a retiree with a large balance in a pre-tax account such as an IRA or 401(k), these RMDs can bump up a retiree’s income to a point where they are assessed the surcharge.

A common scenario where IRMAA can be triggered is when a spouse passes away. When this happens, the surviving spouse will lose the lower of the two spouses’ Social Security benefits, and potentially inherit their spouse’s IRA. Because the surviving spouse goes from Married filing status to Individual, their tax brackets are accelerated and can end up paying more in tax even if their income goes down. This is commonly referred to as the widow’s penalty.

2. Plan for Healthcare Costs

Along with education costs, healthcare costs have increased at one of the highest rates of any of the expenditures in our economy. Just like with investing for retirement, smart planning for these expected increases is one of the best ways to prepare for higher inevitable expenses in retirement.

A common way to take control of healthcare costs is through the use of a Health Savings Account(HSA). HSAs provide triple tax benefits and are a useful tool to use as a buffer against rising healthcare costs—here’s how:

- Savings Opportunities: For someone who is nearing retirement, HSAs can be a great vehicle to put extra savings, as the likelihood of needing funds for healthcare expenses will most likely be a sooner likelihood than someone who is in their 20s or 30s.

- Tax Deductions: The deductions that you can receive on contributions made into an HSA are a huge benefit. Many pre-retirees are in their peak earning years where tax deductions are the most valuable. In addition, someone who is over 55 is allowed a catch-up contribution of $1,000. Combined with the annual family maximum of $8,550 in 2025, someone can receive a tax deduction of up to $9,550 against their income.

Along with ongoing healthcare costs, long-term care costs are also a large expense for many retirees in their later years of life. According to Genworth, the cost of care for a private room in a nursing home in Billings, MT is over $8,000/mo. Without long-term care insurance, these costs can erode a retiree’s portfolio extremely quickly.

Addressing the potential for long-term care costs early is an important consideration for pre-retirees. The costs of long-term care insurance can become cost-prohibitive once someone reaches their mid-60s. Therefore, it is important for pre-retirees to examine what their potential costs will look like, preferably while they are still in their 50s. This can include history of medical care, family longevity, current assets, and likelihood for family assistance.

3. Investment Management

Proper investment management is one of the pillars of the best retirement planning. If an investment account is opened, yet never invested or monitored, it can quickly become an underperforming asset that could otherwise help to contribute towards an enjoyable retirement.

A good financial planner will help with many or all of the following: determine proper risk tolerance and time horizon, conduct periodic rebalancing, review suitable investment choices, and align your investment goals with your overall objectives.

Proper allocation of funds to the right types of accounts is also an important part of investment management. This is referred to as Tax Location. Because different types of accounts are taxed differently, it is important to place the right assets in the places they are utilized best. This results in the best after-tax return on your investments. For an in-depth explanation of tax-efficient investing, check out a recent blog post and webinar.

Another major consideration as it relates to investment management is the necessity of planning for higher inflation and longer life expectancy. We’ve seen the effects of higher inflation over the last 2-3 years, and it’s no wonder that it is referred to as “the hidden tax”. When our dollar doesn’t go as far, it’s harder to keep expenses under control, which impacts the amount of money that we can save or invest.

Living longer is also another “hidden” cost that needs to be factored into a good retirement plan. While we tend to like the idea of living longer, the reality of needing to plan for a longer retirement of potentially 20-30 years adds additional complexity and risk. It is a general practice to become more conservative with age. However, if retirement can last several decades, it might be necessary to maintain a growth allocation for part of your assets to ensure they continue to outpace inflation and ensure you don’t outlive your money. This is where segregating the appropriate assets that aren’t needed in the short term is important.

4. Setting Realistic Goals

Goal setting is where I see the biggest lack of attention in retirement planning. Spending time contemplating what you want to do and where you want to spend retirement are important considerations as you plan for how to get there. However, far too many retirees don’t spend nearly enough time identifying their retirement goals. This can lead to unproductive planning, as the “goalposts” keep constantly shifting.

When goal setting, it’s important to think of the process as a pyramid. While many people want to jump right away to the financial and quantitative part of planning, that shouldn’t happen until the foundation has been laid first. As mentioned in the last paragraph, the majority of time and energy should be spent on the first two steps of goal setting, which are identifying and prioritizing the goals that are most important.

From there, it becomes much easier(and quicker) to decide on the goals that are most important, as the foundation has been laid.

Once someone decides on their preliminary goals and moves to implement them, there is a very high probability of needing to adjust their goals at some point down the road. This is where a financial planner can help to further refine and adjust as desires and goals change.

A few examples of these adjustments include talking through deeply rooted concepts such as purpose, fulfillment, and giving back. While these may not seem like topics a person should be talking with a financial planner about, these conversations can truly help to align deep convictions and emotions with something as unemotional as money.

Another way a financial planner can help someone plan for retirement is through giving “permission” to take one or multiple “test” retirements. For example, if a retiree is considering relocating to a warmer state in the winter, a financial planner might encourage the person to take 3 months and spend the money necessary to “test out” the location and lifestyle they are envisioning long-term. This allows the retiree to get a firsthand experience of what it’s like to be in that environment without making a long-term commitment.

5. Charitable Giving

While this isn’t always a mandatory part of a retirement plan, knowledge of charitable giving strategies can help to link a retiree’s giving goals, tax strategy, and income/distribution strategies.

One of the major benefits for those who are charitably inclined is the various tax advantages that become available for retirees. For instance, an individual who is 70 ½ or older can donate up to $100,000 per year from their IRA tax-free to a charity of their choice. This is known as a Qualified Charitable Distribution.

This giving strategy achieves two valuable advantages:

1) The distribution goes towards fulfilling the Required Minimum Distribution(RMD)

2) The money given to charity is excluded from income.

Since the money in the IRA was originally deducted from income, this money given achieves a double tax benefit. For more details on this strategy, please see our blog post on Tithing Strategies for Charitable Giving.

One of the ways a financial planner can help a future retiree maximize their charitable giving strategy is through reverse QCD planning. Reverse QCD planning is a method by which a retiree determines the amount they wish to give to charity in retirement, and the financial planner helps them to fund and/or grow an IRA to an amount that will produce the annual amount they would like to give to charity. In this way, the future retiree optimizes the amount of the tax deduction that they will be receiving now as well as the ideal amount they will be able to exclude from their income in retirement.

A second charitable giving strategy a financial planner can help with is charitable bequest planning. This involves determining how much the retiree would like to bequeath to the charity upon their death and working backwards to determine how much growth and/or contributions need to be used to fund an IRA to achieve the appropriate balance.

Because IRA contributions are tax-deductible, the retiree receives a tax deduction on the amount they have with the IRA. In addition, the charity can then withdraw the proceeds from the IRA income-tax-free due to their non-profit status.

Moreover, charitable bequest planning allows a retiree to benefit their personal heirs more by designating tax-favorable accounts to them as opposed to pre-tax accounts such as IRAs. For example, let’s say a retiree has two kids, a Roth IRA worth $200,000, a Traditional IRA worth $100,000, and would like to bequeath $100,000 to each of his two kids and $100,000 to his alma mater.

If he gave any of the money in his Traditional IRA to his two kids, they would pay income tax upon withdrawal of the money. However, if he gave the money in his Roth IRA to his kids, they would receive the withdrawals tax-free due to the Roth IRA status.

Therefore, instead of equally dividing the two accounts among the three beneficiaries, it would be more tax-favorable for everyone if he bequeaths the $100,000 IRA to his alma mater and split the $200,000 Roth to each of his two kids. In this way, all of his heirs receive a tax-free inheritance and he minimizes the amount of tax both he and his heirs pay.

Simplify Your Retirement Planning

When choosing a partner for something as important as your finances, transparency is a must. At Evergreen, we approach financial planning biblically—our stewardship minded approach stems from our belief that these are God’s resources and we’re just managers of them.

We’re not a disconnected business partner. Our relationship-centered approach means we’re alongside you on this journey to financial health and retirement planning. If you’re looking for a financial partner who is invested in your success, schedule a meeting with us today. We’d love to meet you!

Interested in working with us?

Schedule A CallKnow someone who might be interested in working with us?

Fill out our referral formThis content is developed from sources believed to be providing accurate information. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security. Evergreen Financial Group, LLC is a registered investment advisor offering advisory services in Montana, Utah, Wyoming and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training. This communication is for informational purposes only and is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision. All opinions and estimates constitute Evergreen Financial Group’s judgement as of the date of this communication and are subject to change without notice. Evergreen Financial Group does not warrant that the information will be free from error. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk.